Smoothing parameter selection criteria for penalized likelihood inference in semiparametric simultaneous joint equation models with correlated random effects

Jan 15, 2026· ,·

0 min read

,·

0 min read

Anderson Bussing

Giampiero Marra

Abstract

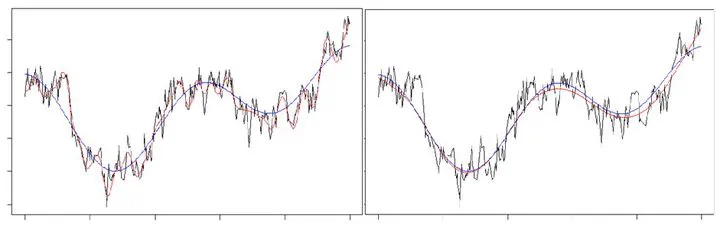

An adjusted UBRE smoothing parameter criterion is sought for simultaneous joint equation models with unmodeled correlated random effects in parameters’ linear predictors. Traditional UBRE criterion leads to undersmoothing in this misspecified case as it interprets wiggliness from the unmodeled random effect as signal to be modeled.

Type

Publication

Working Paper